MURDER, POLITICS, AND THE END OF THE JAZZ AGE

by Michael Wolraich

Yesterday there was a rally in front of the 22nd District Court in Inkster, Michigan, where foreclosure proceedings were being held. The protesters were there to help save the home of Jerome Jackson, a paraplegic who moved into his wheelchair-accessible home in 2004 with the assistance of Community Living Services, a county-funded program that provided help with his mortgage payments. When CLS dropped Jackson's funding in 2009, he fell behind on his payments and Fannie Mae eventually bought his mortgage at a foreclosure auction. He was a man without a home, but he stayed put, hoping they could work it out and the house might someday be his again.

No amount of pleading could sway the steadfast bottom-liners from moving toward the day when Jerome Jackson would finally be evicted. No addition funding came his way, even though he is handicapped and certainly qualifies. Payment modification appears to have been out of the question. The house now belongs to an entity given personhood by our Supreme Court without also having given it a heart.

A story told many times before, most often with a less-than-happy ending, but Jerome Jackson isn't fighting his battle against the Big Guys alone. A loose coalition made up of UAW Local 600 and members of three local groups--Occupy Detroit, Moratorium Now, and People Before Banks--have taken up the cause and are responsible for organizing this rally (and others, as needed):

The banks were bailed out for their reckless profiteering

and fraudulent practices because they were “too big to fail.”

Jerome Jackson is “too human to discard.”

Whatever the outcome, let it be said that the people tried.

There was a time when we might have read this story and moved on, saddened by the prospect but generally acknowledging that--poor man--what's done is done. We've been there, we've done that, over and over again. What we're left with are numbers of foreclosures and evictions across the country so unbelievable it feels like something out of a depression-era novel. What we're left with is a whole lot of suffering, the causes of which smack suspiciously of callous profiteering, alternately smacking of outright criminal cruelty.

Much of my own state, Michigan, is struggling with heavy foreclosure rates, but in Detroit the statistics are especially grim. Roger Bybee put it into perspective in his "In These Times" piece yesterday:

Abysmal poverty afflicts the city; 40,000 households have suffered water shutoffs. The specter of thousands of new home foreclosure stalks the city, threatening to push more Detroiters out of their homes on top of the 67,000 bank foreclosures—more than 20 percent of all household mortgages—that hit the city between 2005 and 2009 alone. The city already has an estimated 50,000 to 70,000 vacant homes. With the ongoing wave of foreclosures, home values have been plunging. Foreclosed homes sell for $38,000 in Wayne County and less than $11,000 in Detroit, according to RealtyTrac.

Bybee writes of a particular foreclosure effort that didn't follow the norm, thanks to the efforts of caring individuals joining together as a formidable coalition:

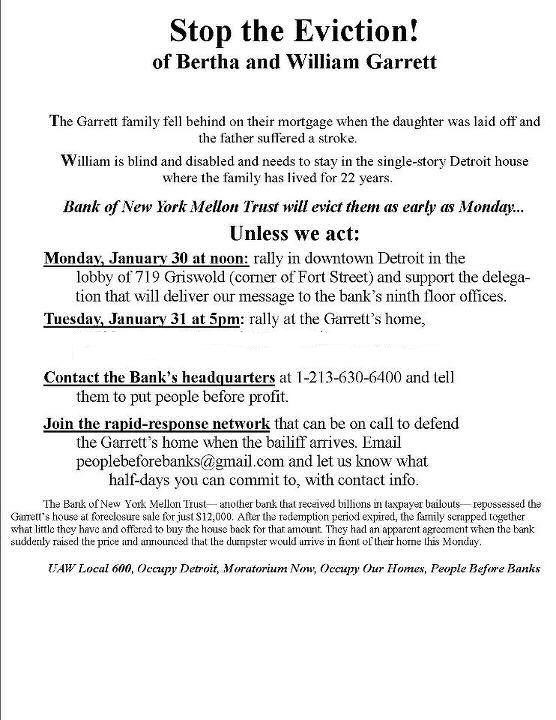

Labor educator Steve Babson, a leader of People Before Banks and author of Working Detroit, recounted a recent action that was “a scene straight out of Charles Dickens." An elderly African-American couple, with husband William legally blind, missed some mortgage payments to the New York Bank of Mellon Trust. In a sheriff’s sale, the bank bought the home for $12,000, meaning that the Garretts would have to move from their home of 22 years in the dead of winter.

At one point, Bertha Garrett thought that she had persuaded the bank to sell the home to the Garretts for the $12,000 that the couple had managed to scrape together. But then the bank backed out of the deal, insisting on a sale price of $24,000, far out of reach for the couple.

Usually, what happens next step in the foreclosure process is the arrival of a truck hauling a dumpster, with a crew ready to throw out a family’s belongings. But UAW 600 and its allies confronted the would-be eviction team with a tactic appropriate to the Motor City: cars and lots of them. The anti-foreclosure forces surrounded the Garretts’ home with dozens of cars, and the bank’s evictors were shut out. When the eviction squad called in the police, officers came to the scene but dismissed it as a “civil matter” and drove off. That left the anti-foreclosure forces still in command of the situation, and the evictors left the scene.

Meanwhile, some 40 protesters—about half from Local 600—picketed outside the Mellon bank to publicize its treatment of the Garretts. With the eviction foiled and the prospect of bad publicity growing, the Mellon bank relented and sold the Garretts’ home back to them for $12,000.

(NOTE: No, I don't know how the Garretts came up with the needed $12,000. I've anticipated that question from the folks who think all economic victims got that way on purpose, so here's my answer: I'll bet my life that they weren't hiding it under their mattress, waiting to pull it out just in the nick of time, guaranteeing a rip-roaring miracle of a finish to what seemed in the early scenes like a real tragedy. The point, you ninnies, is that the bank reneged on an agreement and asked for double the amount, just because they could.)

Attempts to stop foreclosure actions are taking place all over the country. One particularly innovative way is to sing it. This video is from a courtroom in New York, but the "Mr. Auctioneer" song is traveling fast and is now being sung in rallies and in foreclosure courts all across the nation. (Rachel Maddow's take here.)

Mr. AuctioneerAll the people hereAre asking you to stop all the sales right nowWe’re going to survive, but we don’t know how

|

| Foreclosure protest singers being led out of a NY courtroom |

Is this just the start of something big? Or is it already big?

It appears to be big. People are gathering in organized protests in all corners of the country and the word "occupy" is taking on a whole new meaning. It's not just about Wall Street anymore. It's moved to our cities, our towns, our neighborhoods. It's about where we live and how we live and who gets to decide.

Everywhere there are coalitions forming to combat the coalitions intent on keeping the Honkin' Big Bonanza going, but to see what's happening locally you need look no further than the nearest union hall. Check out their websites. You'll find deep and abiding involvement in helping members of their communities entrapped in an economy not of their doing and not of their choice. (It's because they're unions, O dubious ones. That's what unions do.)

Have you noticed that it's getting harder and harder to shame people whose only motivation is making tons, and I mean literally tons, of money? They've played the blame-the-victim game for so long they've fine-tuned to perfection the pretense that keeping the über-wealthy happy means riches for us all. Never mind that there hasn't been a single economic indicator in the history of our republic that proves their point. Never mind that we've been keeping the über-wealthy happy at our expense for decades now and all that has happened to make lives better is that the über-wealthy have become ecstatic to the point of permanent giddy.

People are suffering through no fault of their own. Others are not only profiting from their suffering, they're doing everything they can to keep it that way. Now we've taken it upon ourselves to do something about it.

Real people making real change. And for the good. It's just crazy enough to work.

(Cross-posted at Ramona's Voices)

Comments

As one who has professional experience in the facilitation and oversight of consumer loans, this whole foreclosure debacle is illogical, at least on the surface. It just does not 'compute'.

But, if you apply the 'follow the money' rule, much like peeling an onion (the end result is both will make you cry), therein is the rotten core and facts.

I've stated this before, while there are surely a percentage of foreclosures that are always based in the reality that the mortgage holder is and will be unable to make the payments for a variety of valid reasons, making the need for foreclosure inevitable, the majority of these are not within this factor.

I strongly endorse:

But, armed only with societal outrage, their actions will only produce minimal results.

FOLLOW THE MONEY.

by Aunt Sam on Fri, 04/20/2012 - 10:27am

It's always "follow the money" these days, isn't it? I agree that there will always be some foreclosures that are legit because there will always be some people who screw up and bring their problems on themselves, or who lose jobs and have to downsize, etc., but when the foreclosure numbers are as at pandemic level, something's gotta give.

Seems to me the reasons for it have been established. Now the question is, why isn't something being done about it? Why aren't the banks cooperating by dropping charges and modifying mortgages? Why would a bank arbitrarily double the price of a mortgage payoff when they had already agreed to the terms?

I venture it's because there's more money in government bailouts than there is in reinstating a low-interest mortgage.

But again. . .what to do about it?

by Ramona on Fri, 04/20/2012 - 2:50pm

There's also huge profits to be made from speculators/investors who have the means to purchase properties and wait for the turn around. Interesting to cross reference some of the largest ones with shareholders and others who are much less than the touted six degrees of separation.

It's always about money in these instances. The government has not done a very good job in this area, but public pressure has caused a bit of a increase in the intensity of their 'investigations' - but not near enough. The answers are there for those who care enough to do the research.

by Aunt Sam on Sat, 04/21/2012 - 5:26pm

There is definitely more money to be made in the government bailouts. A few years ago, Firstbank (I think it was Firstbank, anyway) was sold to a larger bank, and I want to say that larger bank was USBank but I am not sure.

In any case, as part of the transaction, the bad mortgages were sold in a complex public/private partnership. As I understand it, the terms involved the government chipping in enough to make it worth the private investors' while to take on the bad debt. In this scenario, all the rich folk get to stay whole, the government doesn't take on the entire debt, and the whole thing takes place way over the heads of individual homeowners. Problem fixed, right?

Of course the downside is that any effort to do anything with individual mortgages cuts into the pre-established profits arrived at in said agreement. I don't know if variations on similar agreements are in place for all the mortgages in the country, but if so, it may explain why loan modification appears to be mostly for show, a little red meat thrown down for the occasional deserving old couple with a group of activists behind them, but is not being undertaken on any kind of grand scale. There's just no financial incentive to save anyone's home, even if there are financial incentives being advertised, because the pre-existing bailout is so lucrative. Better to just let the thing "run its course" and let all that money keep on flowing upward.......

At this point, I don't think there is anything to do about it. Many of the people with "trick" mortgages initiated between 2000 and 2005 have already lost their homes or are going to lose them. If there was going to be any organized effort, it should have been to rewrite that group of mortgages. Now the situation has shifted, and much larger numbers of people are losing their homes because of economic troubles stemming from the first mortgage crisis. In my mind, these two crises are different animals, and no politician in his or her right mind would be willing to get behind the kind of forgiveness effort required to solve the problem. The moral hazard people would scream communism like nobody's business.

At this point, from a business standpoint and I make no claim on the relative morality, anyone currently in danger of losing their home is probably going to lose it. They should stop making their payments, use the cash as best they can, figure out how to declare bankruptcy if necessary, and work on figuring out how to live in a post-real-estate world. I know that sounds like a cheesy infomercial, but I think that is where we are right now.

by erica20 on Mon, 04/23/2012 - 12:49pm

Erica, I blame the the problem, on the lack of leadership at the top.

Obama should have been primaried, because of his callousness towards homeowners.

America is screwed, whether we get Romney or Obama.

The money changers get to maintain control with either nominee.

Obama hurt the working class .......TOO .....

and for that he'll get rewarded?

The message ....Go ahead and hurt the working class, just don't do it as bad, as the republicans.

by Resistance on Tue, 04/24/2012 - 7:54am

Resistance, I hear ya. The lack of response from Democrats throughout this crisis has been thoroughly disappointing. And any Democrat who wants to know why certain groups and individuals aren't out there knocking on doors for him or her, only need to look at whether those groups and individuals have lost a house or not.

People tend to take that sort of thing quite personally, and disappear forever from the volunteer lists of politicians they would otherwise support.

by erica20 on Tue, 04/24/2012 - 3:35pm

If you recall, in 2008 we were all encouraged to throw open the doors to the Treasury and allow hundreds of millions of dollars to flow into Wall Street almost overnight! And we were told to hurry on the basis of a four-page "plan" written out by Goldman Sachs, er, I mean our Secretary of the Treasury. This money was supposed to deal with all the "toxic assets" that would surely be a drag on the economy for the foreseeable future, and those "toxic assets" were rightly defined as the inflated asset mortgages that were now under water.

Not hardly a nickel paid or an ounce of attention devoted to individual homeowners subsequent to this. But we did back the bad bets placed at casinos like AIG at 100 cents to the dollar - money that ultimately protected every cent Goldman Sachs had wagered as well.

And now? After taking all our tax dollars to hold themselves harmless, these banks sniff at troubled mortgage holders looking for relief. "Have they no workhouses?" they ask. "Don't they know who's boss here? They will accept OUR terms or have no terms at all!"

We need to stick them all in the neck and bleed these banks like stuck pigs. There is no redemption. We are the 99 percent. Occupy Wall Street. And let them take their bought-and-paid-for political parties - Republican AND Democrat - down with them as well.

by SleepinJeezus on Sat, 04/28/2012 - 4:10am

by Richard Day on Fri, 04/20/2012 - 1:59pm

Thanks for this, Ramona. I appreciate getting details about what is being done in Michigan to confront the banks and the rule of wealth that places profit over justice.

These are encouraging rumblings you describe. There is an air of insurrection that is building on many fronts, just as surely as there has been a well-orchestrated attack on the middle class and the poor that has been underway for the last thirty years. We are treated as cattle, or as simple commodities to be used and traded and discarded in whatever way it serves the greater profit of the owners.

We are pitted one against the other not unlike dogs in a fight. I see this most keenly here in Wisconsin, and it sickens me to my core. I greatly anticipate the day when we "contestants" in this fight become sufficiently aware to look beyond the ring into the eyes of those who own the arena and who now laugh at our miseries and bet upon our misfortunes. I want us to catch them in their corpulence with their throats exposed. I want them gone.

Justice will out. We know this, but it doesn't make these present times any less scary, nor any less exciting. For more than thirty years, we have been under an intense assault. This is Class War, but it only becomes such when we begin fighting back. We are the 99%. Occupy Wall Street.

by SleepinJeezus on Sat, 04/28/2012 - 4:32am

More news on the topic...

by SleepinJeezus on Sat, 04/28/2012 - 6:43am

Wells Fargo--not a romantic stage coach company anymore. How ya doin, Zhukov?

Good to see you around.

by jollyroger on Sat, 04/28/2012 - 7:54am